.png)

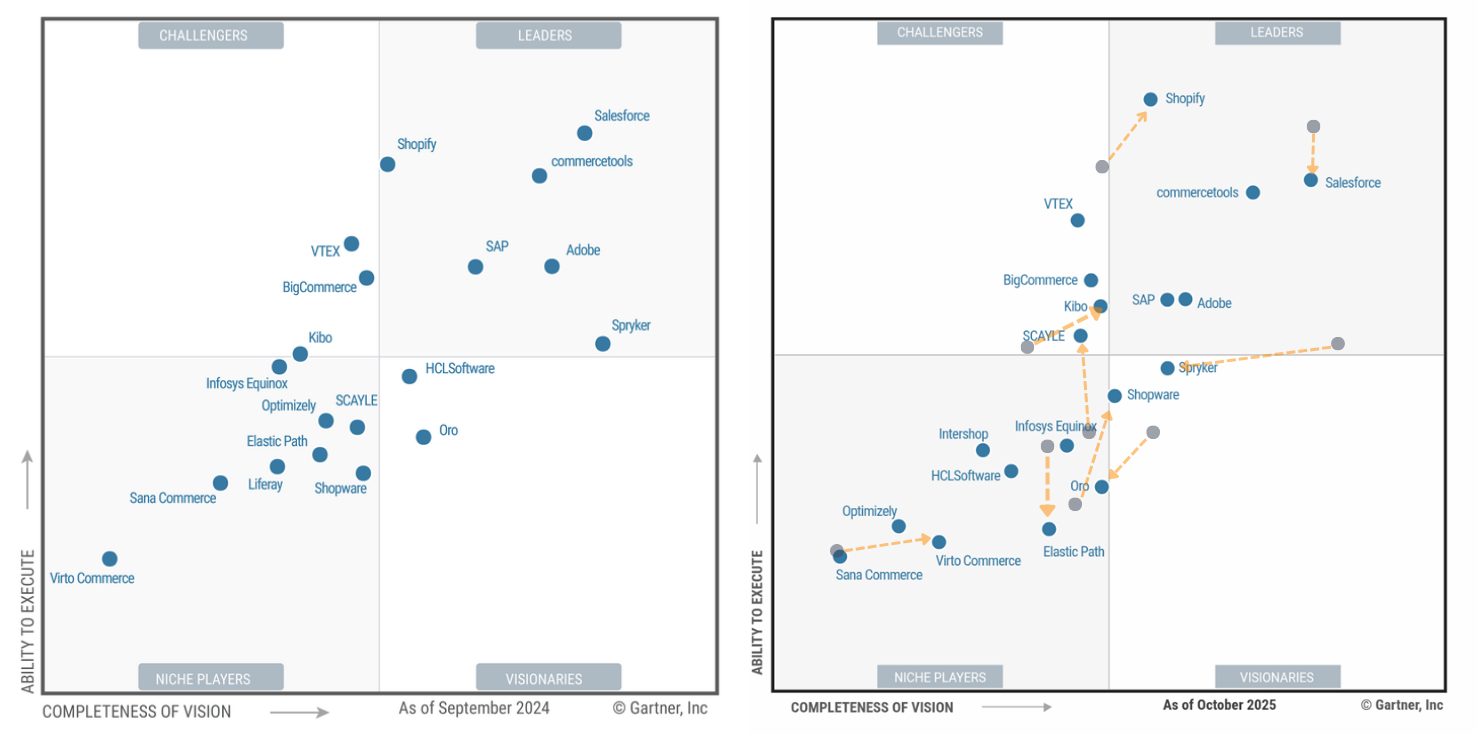

The 2024 Gartner Magic Quadrant captured a moment when many companies were hesitant to make big moves: budgets were tight, teams were cautious, most leaders focused on keeping their commerce systems steady rather than pushing into something new. The thinking at the time was simple - avoid surprises and stick to plans you know you can deliver, upgrade only when the risk feels low.

The 2025 version tells a different story. Companies are spending again, yet they are far more selective about what they adopt. The push for upgrades is no longer about collecting add-on features. The main value is choosing architectures that can adapt without drama, trimming operational drag, and giving business teams more room to manage their own work without constant technical help.

A few themes stand out this year:

The move is not a return to carefree spending. Teams are putting money toward tools that help them move faster without inviting unnecessary risk. This trend is especially visible in how mid-market platforms such as BigCommerce, Shopify, VTEX, and Kibo are evaluated. Their appeal comes from a balance of capability and reasonable cost, paired with a path to implementation that does not swallow months of effort.

The year-over-year movement in the Magic Quadrant shows a market that is settling into a clearer shape. Companies are still maturing their digital commerce strategies, yet they are heading in different directions based on their priorities and operational needs.

Some vendors climbed noticeably. Their progress came from stronger capabilities, steadier adoption patterns, and more mature partner communities: SCAYLE reached the Challenger category for the first time, Shopware moved into the Visionary quadrant. This shift reflects its focus on faster product improvements and a growing network of extensions.

The lines between categories are becoming sharper. Leaders today are defined by their scale across technology, partner depth, and global reach. Challengers show strength in execution and architectural clarity, Visionaries stand out for the pace at which they ship new ideas, Niche Players find their footing by serving specific verticals or offering a tight, well-defined product fit.

In 2024, the Visionary label was sometimes interpreted too broadly. In 2025, it signals something more specific. These are the vendors pushing the edges of modular commerce, workflow design, and tools that give business teams more control. This is different from those that simply serve a narrow industry.

Revenue for 2024 sits in the upper single-digit billions across most estimates. Numbers vary because firms define ‘commerce platform’ differently. Some include only software, and others include implementation work and nearby services. Even so, the general direction is clear. Growth held in 2024 and confidence strengthened moving into 2025.

Together, these shifts paint a picture of a tiered landscape: leadership is no longer only about size, mid-market vendors are proving they can compete effectively, and companies are recognizing that the right fit often comes from a more focused platform rather than the biggest one.

The 2025 Quadrant shows a market where ideas that once sat on the edge of adoption have moved into everyday expectations. Composable setups, for example, have become standard in B2B and mid-market teams that want room to adjust their systems without rebuilding everything from scratch.

Retailers with stores still depend heavily on unified commerce features. They need tools that let physical locations, online shops, and marketplaces share inventory, customer activity, and promotions with as little friction as possible.

AI usage varies across the field. Some vendors focus on search improvements, content support, and workflow prompts. Others are still laying the groundwork. Even so, interest is building as teams look for small but consistent gains they can rely on.

Content management has regained attention. Many organizations want business users to shape experiences on their own. They are tired of waiting in line for technical updates that should be manageable through simpler tools.

Integration quality carries more weight than it once did. Deep connections to ERP, PIM, CRM, and OMS systems often decide which platforms stay on the shortlist. A vendor that cannot tie cleanly into those core systems gets pushed aside early in the process.

Put together, these trends highlight a larger shift. Digital commerce strength depends on the system around the transaction. Flexibility, consistency, and integration depth influence success just as much as what happens at checkout.

The 2025 Leaders list includes Adobe, commercetools, Salesforce, SAP, and Shopify. Each of them approaches digital commerce from a different angle, and that variety shows how broad the market’s needs have become.

Adobe pushed further into cloud-native commerce in 2025. The introduction of its SaaS version of Adobe Commerce, paired with tight links to its creative and content tools, gives it a clearer identity as an experience-driven platform. Its generative engine supports a steady flow of content tasks, and teams that rely on Adobe’s broader suite often find value in having everything under one roof.

commercetools remains one of the strongest examples of modular commerce. The platform keeps widening its set of building blocks, including fresh tools for store environments and early AI orchestration features. Its track record across large implementations helps it stay firmly in the Leader group. Many organizations choose it because they want a setup they can shape over time without heavy constraints.

Salesforce continues to lean on its strengths in data alignment and workflow automation. The commerce side of the portfolio benefits from improvements made across the wider Salesforce platform, which helps teams unify customer activity and internal processes. Its partner community remains one of its biggest advantages, especially for companies that want a wide set of extensions.

SAP holds a strong position among global B2B organizations with complicated operational needs. Its hybrid architecture keeps evolving, especially in areas tied to customer self-service and workflow extensions. Many large manufacturers and distributors stay with SAP because the platform fits the way they already run their businesses.

Shopify continues to build momentum. Its enterprise tier, Shopify Plus, strengthened uptime guarantees and overall reliability. Investments in unified commerce and infrastructure scale have helped it attract more mid-market and enterprise customers. The appeal often comes from its straightforward setup paired with an ecosystem that covers most business needs.

Together, these Leaders offer a wide mix of capabilities and partner support. Their approaches differ, yet each one has a clear path for companies that need strong performance, consistency, and room to grow.

The mid-market space saw some of the most noticeable changes between 2024 and 2025. These platforms now compete with enterprise vendors on capability while offering faster implementation cycles and more manageable costs. Many companies that once assumed they needed an enterprise suite are starting to test that assumption.

BigCommerce remains a standout Challenger and an important option for mid-market B2B teams. Its strengths include a clean, API-first setup, strong support for contract pricing and multisite operations, and availability across major cloud regions. The platform also benefits from Feedonomics, which gives teams a reliable engine for feed management and data prep. BigCommerce has deep connections to PIM, ERP, OMS, and enterprise search systems, which plays a major role in evaluations. This mix makes it attractive to manufacturers and distributors that want to modernize without taking on the weight of a large enterprise stack.

VTEX continues to expand its support for hybrid retail and B2B models. The platform includes collaboration tools for merchandising and content workflows, along with AI features aimed at improving day-to-day efficiency rather than adding complexity. VTEX appeals to companies that want unified commerce inside a single platform setup. Many mid-market merchants choose it because they need both flexibility and a straightforward operating model.

Kibo invests heavily in merchandising, personalization, and forecasting. Retailers that want unified commerce without taking on a large enterprise suite tend to look closely at Kibo. Its architecture supports both composable builds and rich front-end experiences across channels. This gives teams room to experiment while keeping the system manageable.

SCAYLE’s move into the Challenger quadrant shows how far it has come in operational maturity. The platform was built around retail best practices and includes multisite and multi-brand management, along with integrated OMS, PIM, DAM, and mobile app tools. It offers modern merchandising and promotion management and is gaining traction among fast-growing mid-market and upper-mid-market retailers. SCAYLE appeals to teams that want quick deployment times paired with strong capabilities, without breaking their stack into too many pieces.

The Visionary quadrant highlights vendors that move quickly and offer modular setups that teams can adapt without heavy effort. These platforms tend to focus on workflows, business-user tools, and flexible extensions rather than broad industry targeting.

Shopware continues to grow its extension network, which now includes more than 3,000 integrations. The roadmap leans toward workflow improvements, AI-assisted tasks, and stronger international support. Many merchants choose Shopware because the platform gives them room to adjust their setup as their markets shift. Its steady pace of updates keeps it on the radar for companies that want a balance of control and adaptability.

Several vendors in the Niche Player quadrant find success by serving specific industries or regional needs. Some platforms focus on B2B distribution. OroCommerce fits this group with support for quote-driven workflows, buyer-specific pricing, and large catalogs. Others stay close to manufacturing and ERP-driven operations. Sana Commerce is an example, often chosen when companies want commerce activity tied tightly to ERP behavior.

A number of these vendors also support regions where tax rules, payment habits, or local integrations require careful handling. Intershop and Virto Commerce tend to appeal to organizations with long-running operational models that need stability more than broad coverage. Elastic Path also fits here, offering modular tools for companies that want more control over the experience layer.

Their strength comes from understanding customers with very specific patterns. They follow the daily challenges of those organizations, whether that involves field sales, replenishment cycles, or product relationships that change often. This makes them appealing to companies that want tools shaped around their operations rather than a wide feature catalog.

The 2025 Quadrant gives buyers a clearer set of priorities. Many companies are moving away from long feature checklists and paying closer attention to how well a platform fits into the rest of their systems. A few themes stand out:

Interoperability comes first:

Practical AI matters more than broad promises:

Mid-market platforms offer stronger options:

Fit outweighs size:

The 2026 landscape is starting to take shape, even though the Quadrant does not publish formal predictions. The patterns visible in 2025 point toward several directions that are already gaining momentum:

Taken together, these shifts suggest that 2026 will not be about expanding for the sake of expansion. It will center on tighter operations, stronger workflows, and platforms that help teams move with less friction. Leaders want tools that support steady progress, help teams respond faster, and keep long-term plans flexible.

The direction is clear. Success in 2026 will belong to organizations that pick platforms able to adapt without slowing them down, and that treat commerce as part of a larger operational system rather than a standalone project.

Read more insights in our article about Gartner’s 2024 Digital Commerce Report.

Have questions or need assistance with your project? Contact our team, and we’ll be happy to help.